Many employers assume the more people they invite to a workers' compensation claim review, the more …

Who Should Be in Your Workers’ Comp Claim Review Meetings?Read More

![]()

Reduce Workers Compensation Costs By 20-50%

Many employers assume the more people they invite to a workers' compensation claim review, the more …

Who Should Be in Your Workers’ Comp Claim Review Meetings?Read More

Many employers spend most of their workers' compensation management efforts reacting to individual …

How Regular Claims Reviews Help Employers Avoid Costly SurprisesRead More

In this final part of our series exploring the nine elements of independent premium audits, we turn …

Part 3: Workers’ Comp Independent Premium Audits ExplainedRead More

In this three-part series, we are examining nine elements of independent premium audits to help you …

Part 2: Workers’ Comp Independent Premium Audits ExplainedRead More

When an employer receives a revised workers' compensation premium bill, the accuracy of the bill …

Part 1: Workers’ Comp Independent Premium Audits ExplainedRead More

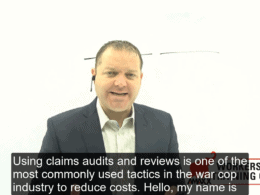

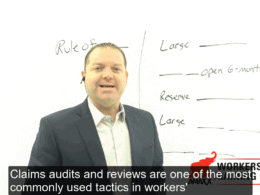

Claims audits and reviews are one of the most commonly used tactics by companies to control …

Workers’ Comp Claims Audit: Initial Action Plan ChecklistRead More

When managing workers’ compensation, a claim audit or review is a crucial opportunity for …

Best Practices to Prepare for a Workers’ Comp Claim Audit or ReviewRead More

One thing seldom heard from the insurance company or the third-party claims administrator (TPA) is …

20 Common Adjuster Mistakes And What To Do About ItRead More

There is an understandable need for workers' compensation internal audits for the self-insured …

File reviews can be an effective tool in reducing workers’ compensation program costs. This is a …

File Reviews: The Who, What, When, Where, and How to Conduct OneRead More

Based on the claims office's performance (or lack thereof), you have determined it would be in your …

Your Roadmap To A Successful Workers Compensation Claims AuditRead More

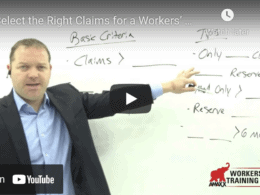

Selecting the right claims for a workers' comp claim audit can make your time much …

Select the Right Claims for a Workers’ Comp Claim Audit Category Claim Audits & File ReviewRead More

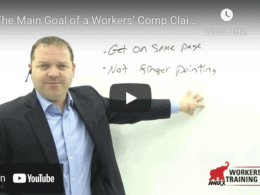

There's one type of meeting in Workers' Compensation thats more valuable than …

The Main Goal of a Workers’ Comp Claim Audit or ReviewRead More

This post is one in a 3-part series: Part 1: Stop Wasting Time Doing Workers' Comp Claim …

Part 3: What to Do AFTER a Workers’ Comp Claim AuditRead More

This post is one in a 3-part series: Part 1: Stop Wasting Time Doing Workers' Comp Claim …

Part 2: Select the Right Claims for a Workers’ Comp Claim AuditRead More

This post is one in a 3-part series: Part 1: Stop Wasting Time Doing Workers' Comp Claim …

Part 1: Stop Wasting Time Doing Workers’ Comp Claim AuditsRead More

This post is one in a 3-part series: 6 Ways to Make Workers' Comp Claims Audits/Reviews …

One Tip To Make Claims Reviews an Effective Use of TimeRead More

Self-insured employers can have a good safety program, an established return-to-work program and …

16 Point Checklist To Determine If You Need A Workers’ Comp Claim AuditRead More

Self-insured employers, insurers, third party administrators, and government entities all use …

How To Get the Most From A Workers Compensation Claim File AuditRead More

A claims auditor was brought in because a self-insured employer was seeing an acceleration …

19 Points to Cover in a Proper Workers’ Comp Claim InvestigationRead More